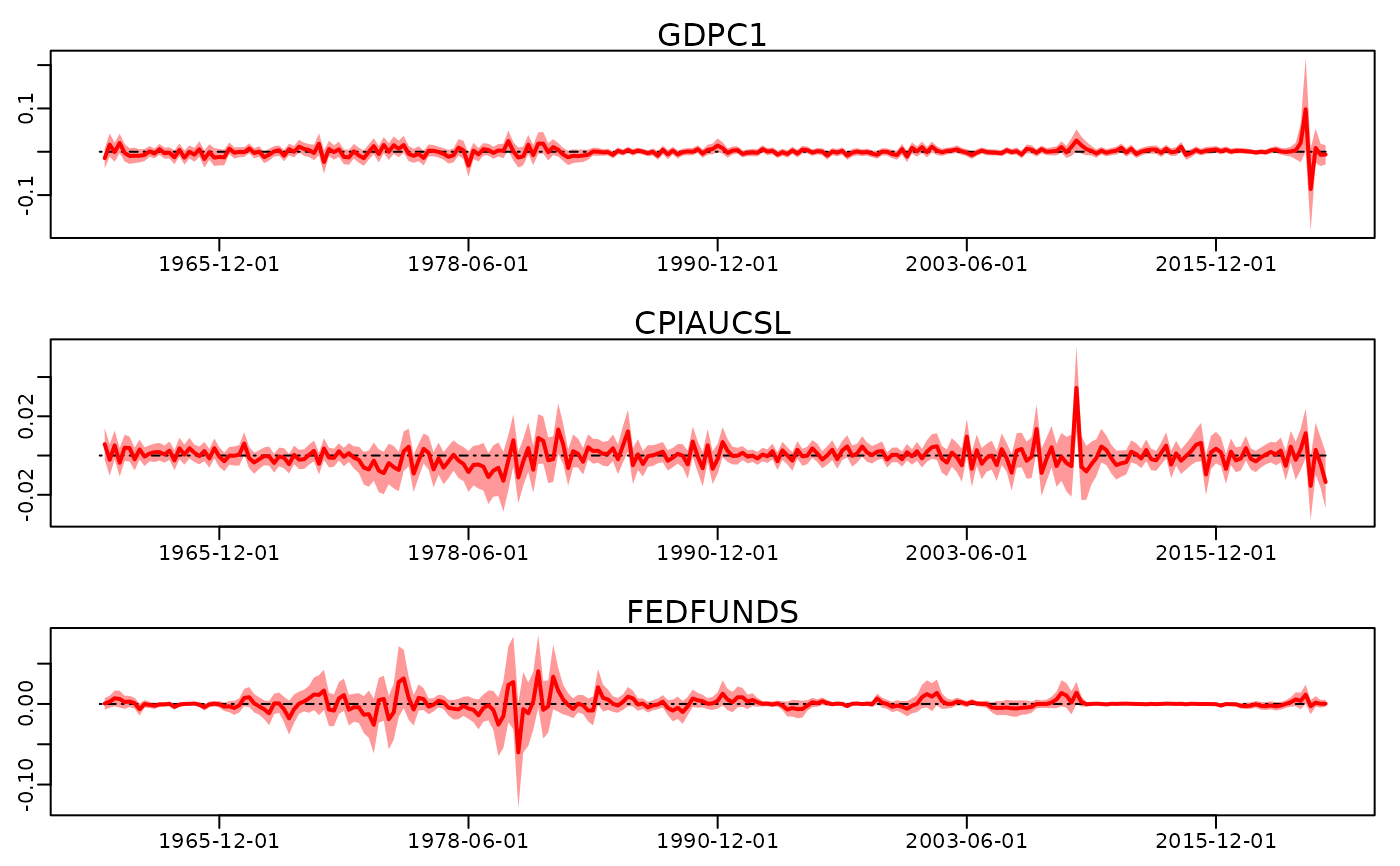

Extract model residuals, defined as the difference between the observed time-series and the in-sample predictions of the VAR model. Because in-sample prediction is subject to uncertainty of the VAR parameter estimates, this uncertainty carries over to the model residuals.

Usage

# S3 method for class 'bayesianVARs_bvar'

residuals(object, ...)Arguments

- object

A

bayesianVARs_bvarobject estimated viabvar().- ...

Passed to

fitted.bayesianVARs_bvar().