Simulates from (out-of-sample) predictive density for Bayesian VARs estimated

via bvar() and computes log predictive likelhoods if ex-post

observed data is supplied.

Usage

# S3 method for class 'bayesianVARs_bvar'

predict(

object,

ahead = 1L,

each = 1L,

stable = TRUE,

simulate_predictive = TRUE,

LPL = FALSE,

Y_obs = NA,

LPL_VoI = NA,

...

)Arguments

- object

A

bayesianVARs_bvarobject, obtained frombvar().- ahead

Integer vector (or coercible to such), indicating the number of steps ahead at which to predict.

- each

Single integer (or coercible to such) indicating how often should be drawn from the posterior predictive distribution for each draw that has been stored during MCMC sampling.

- stable

logical indicating whether to consider only those draws from the posterior that fulfill the 'stable' criterion. Default is

TRUE.- simulate_predictive

logical, indicating whether the posterior predictive distribution should be simulated.

- LPL

logical indicating whether

ahead-step-ahead log predictive likelihoods should be computed. IfLPL=TRUE,Y_obshas to be specified.- Y_obs

Data matrix of observed values for computation of log predictive likelihood. Each of

ncol(object$Yraw)columns is assumed to contain a single time-series of lengthlength(ahead).- LPL_VoI

either integer vector or character vector of column-names indicating for which subgroup of time-series in

object$Yrawa joint log predictive likelihood shall be computed.- ...

Currently ignored!

Value

Object of class bayesianVARs_predict, a list that may contain the

following elements:

predictionsarray of dimensionsc(length(ahead), ncol(object$Yraw), each * dim(object$PHI)[3])containing the simulations from the predictive density (ifsimulate_predictive=TRUE).LPLvector of lengthlength(ahead)containing the log-predictive-likelihoods (taking into account the joint distribution of all variables) (ifLPL=TRUE).LPL_univariatematrix of dimensionc(length(ahead), ncol(object$Yraw)containing the marginalized univariate log-predictive-likelihoods of each series (ifLPL=TRUE).LPL_VoIvector of lengthlength(ahead)containing the log-predictive-likelihoods for a subset of variables (ifLPL=TRUEandLPL_VoI != NA).Yrawmatrix containing the data used for the estimation of the VAR.LPL_drawsmatrix containing the simulations of the log-predictive-likelihood (ifLPL=TRUE).PL_univariate_drawsarray containing the simulations of the univariate predictive-likelihoods (ifLPL=TRUE).LPL_sub_drawsmatrix containing the simulations of the log-predictive-likelihood for a subset of variables (ifLPL=TRUEandLPL_VoI != NA).

Examples

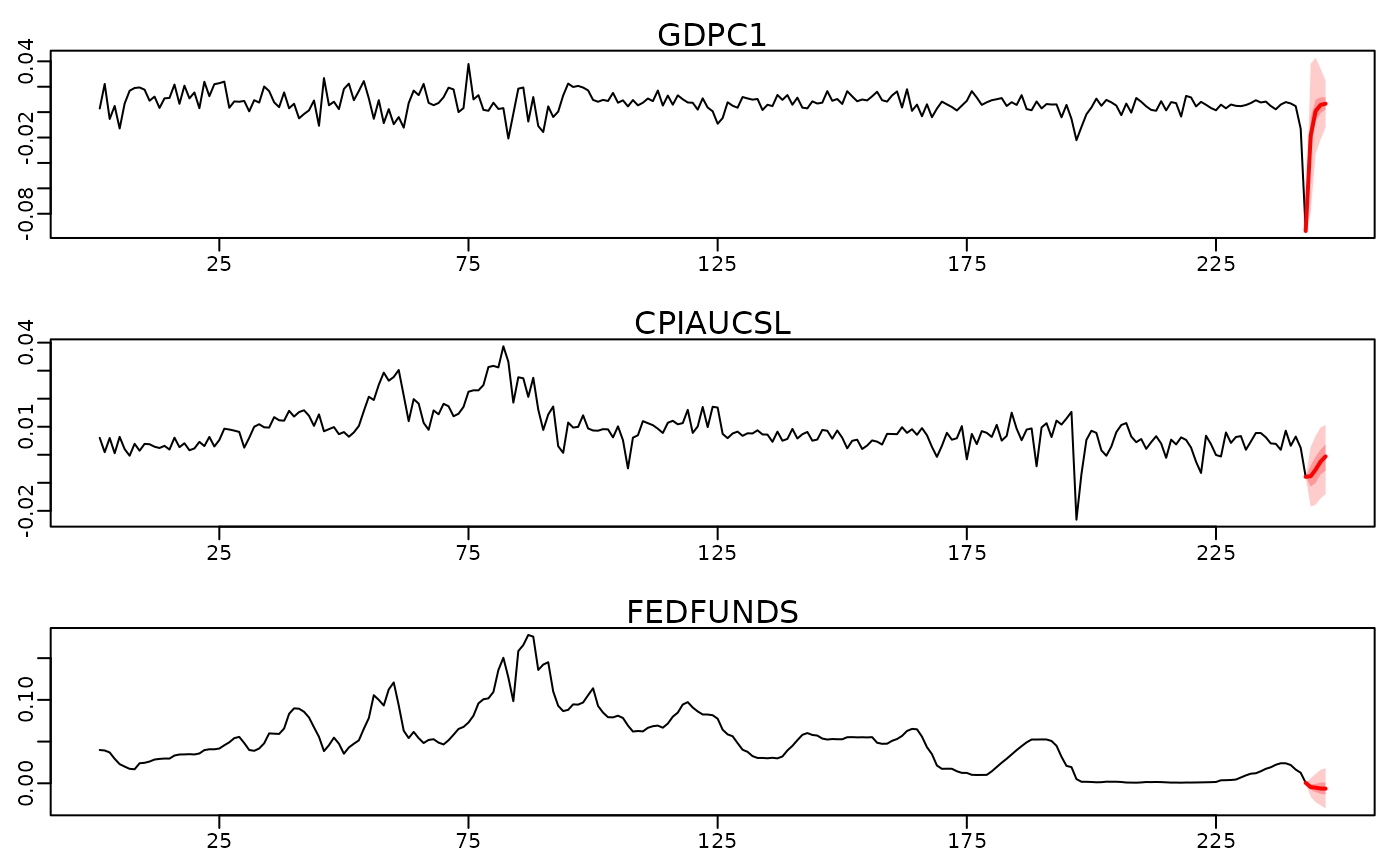

# Access a subset of the usmacro_growth dataset

data <- usmacro_growth[,c("GDPC1", "CPIAUCSL", "FEDFUNDS")]

# Split data in train and test

train <- data[1:(nrow(data)-4),]

test <- data[-c(1:(nrow(data)-4)),]

# Estimate model using train data only

mod <- bvar(train, quiet = TRUE)

# Simulate from 1-step to 4-steps ahead posterior predictive and compute

# log-predictive-likelihoods

predictions <- predict(mod, ahead = 1:4, LPL = TRUE, Y_obs = test)

#> 'stable=TRUE': Calling 'stable_bvar()' to discard those posterior

#> draws that do not fulfill the stable criterion.

#>

#> 490/1000 stable posterior draws remaining for prediction!

# Summary

summary(predictions)

#>

#> LPL:

#> t+1 t+2 t+3 t+4

#> 3.295 8.963 8.848 6.618

#>

#> Marginal univariate LPLs:

#> GDPC1 CPIAUCSL FEDFUNDS

#> t+1 -1.208 0.4945 3.705

#> t+2 2.811 2.7032 3.380

#> t+3 2.986 2.5687 3.225

#> t+4 3.086 0.4691 3.077

#>

#> Prediction quantiles:

#> , , GDPC1

#>

#> t+1 t+2 t+3 t+4

#> 5% -0.06271 -0.0358741 -0.025896 -0.021977

#> 50% -0.01847 0.0003222 0.007422 0.007056

#> 95% 0.03786 0.0396699 0.042156 0.041783

#>

#> , , CPIAUCSL

#>

#> t+1 t+2 t+3 t+4

#> 5% -0.018501 -0.018386 -0.016577 -0.013903

#> 50% -0.008211 -0.005274 -0.002744 -0.001245

#> 95% 0.003095 0.006904 0.010319 0.010655

#>

#> , , FEDFUNDS

#>

#> t+1 t+2 t+3 t+4

#> 5% -0.017187 -0.029766 -0.035690 -0.046158

#> 50% -0.002658 -0.003953 -0.004949 -0.005525

#> 95% 0.014293 0.020864 0.026225 0.028602

#>

# Visualize via fan-charts

plot(predictions)

# \donttest{

# In order to evaluate the joint predictive density of a subset of the

# variables (variables of interest), consider specifying 'LPL_VoI':

predictions <- predict(mod, ahead = 1:4, LPL = TRUE, Y_obs = test, LPL_VoI = c("GDPC1","FEDFUNDS"))

#> 'stable=TRUE': Calling 'stable_bvar()' to discard those posterior

#> draws that do not fulfill the stable criterion.

#>

#> 490/1000 stable posterior draws remaining for prediction!

predictions$LPL_VoI

#> t+1 t+2 t+3 t+4

#> 2.405161 6.277865 6.228728 6.194043

# }

# \donttest{

# In order to evaluate the joint predictive density of a subset of the

# variables (variables of interest), consider specifying 'LPL_VoI':

predictions <- predict(mod, ahead = 1:4, LPL = TRUE, Y_obs = test, LPL_VoI = c("GDPC1","FEDFUNDS"))

#> 'stable=TRUE': Calling 'stable_bvar()' to discard those posterior

#> draws that do not fulfill the stable criterion.

#>

#> 490/1000 stable posterior draws remaining for prediction!

predictions$LPL_VoI

#> t+1 t+2 t+3 t+4

#> 2.405161 6.277865 6.228728 6.194043

# }